Last spring and summer, the Republicans stumbled in their efforts to repeal and replace Obamacare. But they might try a new approach later this year. If they do, expect to hear more debates about what their replacement plans mean for chronically ill Americans. People with pre-existing conditions might get priced out of insurance. People without insurance might delay important medical care, and suffer accordingly. These are serious problems, and Republicans ought to explain what they will do to avoid harming so many people.

But lest you think it is only the poor and downtrodden who will be harmed by this legislation, consider what will happen to your favorite local hospital. Without paying customers – i.e. people with insurance – it is going to lose money. That means even if you are not at risk for losing your insurance, you might lose the ability to go to your neighborhood hospital.

Consider the impact of Medicaid cuts on hospitals. Some Republicans already refused to expand Medicaid under Obamacare. If Republican healthcare legislation becomes law, those states that already expanded will probably be forced to contract their programs. That is going to cost hospitals lots of money, in the form of uncompensated care. When people without insurance become grievously ill, hospitals are required to provide them with emergent care, even if they have little chance of being reimbursed for that care.

(To read the rest of this article, please visit Forbes.)

Rep. Raul Labrador (R-ID) speaks with members of the media at Trump Tower December 12, 2016 in New York. / AFP / KENA BETANCUR (Photo credit should read KENA BETANCUR/AFP/Getty Images)

Back in May, an angry constituent asked Congressmen Raul Labrador why he voted for the Republican House Healthcare Bill, that the constituent claimed would cause people to die for lack of Medicaid funding. The Freedom Caucus member shot back with a now infamous retort: “Nobody dies because they don’t have access to healthcare.” Amidst backlash over what he now describes as an inelegant statement, Labrador tried to clarify his remarks: “I was trying to explain that all hospitals are required by law to treat patients in need of emergency care regardless of their ability to pay, and that the Republican plan does not change that.”

But Labrador forgot to mention that, although hospitals are required to treat emergently ill patients regardless of ability to pay, they are also allowed to bill those patients for that care. That means people without insurance often find themselves either avoiding emergency rooms altogether, or driving long distances to hospitals known for being more forgiving of medical debt. Labrador overlooked the life-threatening risks that financially strapped people take to keep out of medical debt.

Insurance sometimes saves lives by enabling people to get emergency care close to home, without fear of financial insolvency.

This travel-and-die phenomenon is not what most insurance enthusiasts think about when they say insurance improves health. Instead, they talk about how insurance makes people more likely to receive the primary care that prevents life threatening illnesses – mammograms and colonoscopies; blood pressure pills and flu shots. They point out that patients with insurance are more likely to see doctors when they start developing worrisome symptoms. With insurance, the cost of a cardiology appointment no longer stands in the way of getting that “heartburn” checked out. In short, insurance improves health and saves lives by being the difference between whether or not people receive lifesaving medical care.

(To read the rest of this story, please visit Forbes.)

When Lorie Duff was pregnant with her third child, she did what all good moms are supposed to do. She went to the ObGyn clinic for prenatal care. But she fell behind on the clinic payments. She only made about $25,000 a year managing an auto parts store while her husband stayed home with their kids. The out-of-pocket expenses were outpacing her ability to pay.

That’s when she found herself on the phone with a debt collector, who demanded a minimum of $400 to help her out. She knew if she didn’t do that, things would get even uglier. She was in a state of panic, with collectors calling almost every day to wrestle money from her. She was convinced the next caller would inform her she had lost her house.

Unknown to Duff, she was eligible for financial assistance from the hospital, which had turned her unpaid bills over to a collection agency. If she had expressed her financial concerns to the hospital earlier on, she never would have found herself in a position where every time she saw a stranger walking in her neighborhood, she worried it was a repo man.

In normal consumer markets, people owe what they owe. In fact, consumers often can’t purchase goods or services until they pay for them in advance. But in healthcare, patients usually receive services before paying the bill, often (as we’ve seen) before even knowing the price of those services. In part, this backwards relationship between payment and receipt of services occurs because patients require urgent treatment, and providers don’t want to take time collecting money before taking care of their illness. Other times it is backwards because providers send the initial bill to an insurance company, not knowing how much insurance will pay versus how much the patient will be responsible for.

(To read the rest of this article, please visit Forbes.)

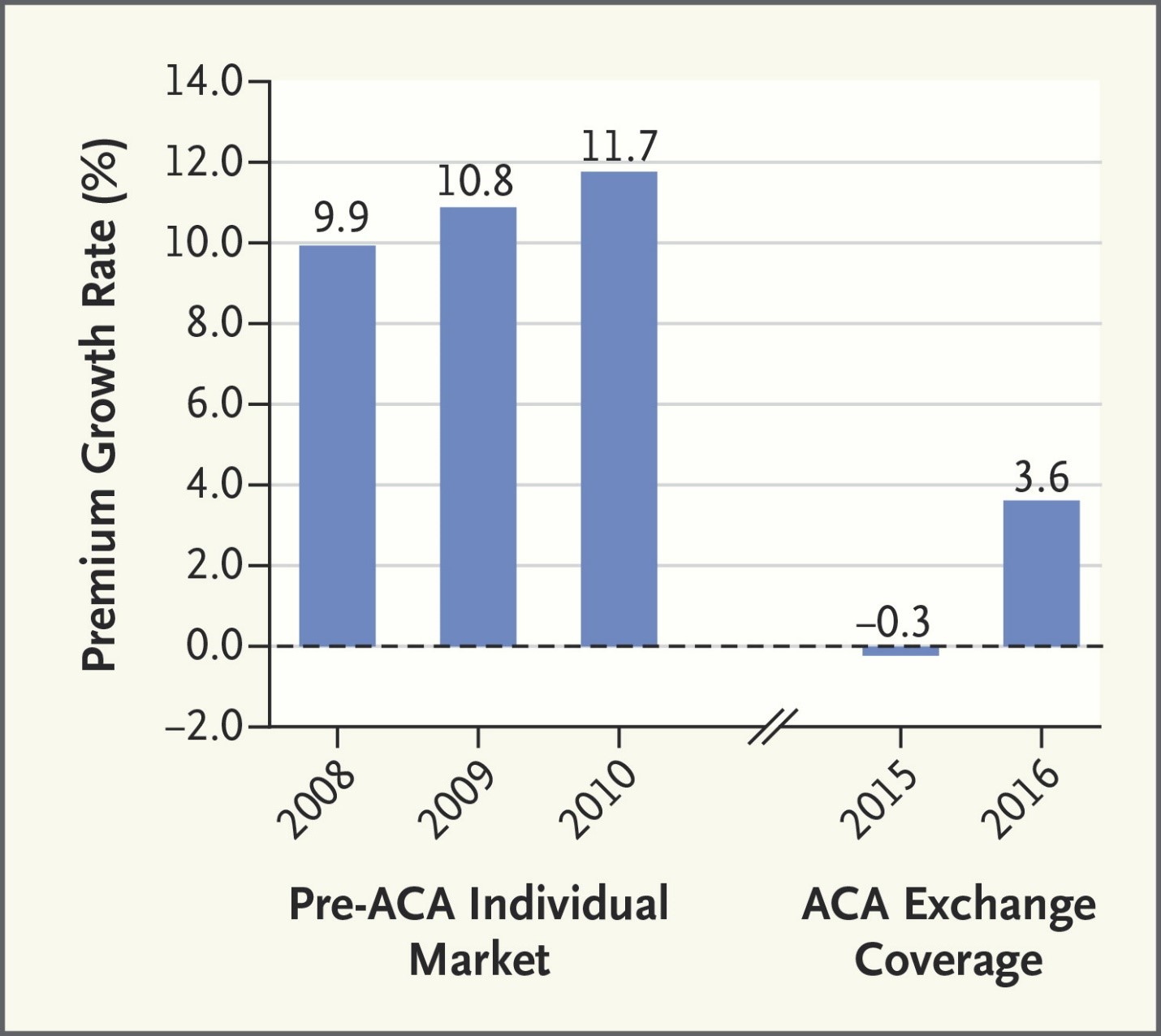

Here’s a picture from a New England Journal of Medicine article showing that in 2015 and 2016, Obamacare premiums grew more slowly than private insurance premiums rose before the law came into effect: New England Journal of Medicine

The Obamacare markets are new and unsettled. But so far they aren’t leading to runaway inflation. But what will happen to these markets if the Republicans are able to repeal and delay? Cue the ominous movie music!

Imagine that you are gasping for breath, literally on the verge of death. Then someone injects you with a medicine and – miracle! – you are perfectly healthy again. Would you pay $300 for that injection? The treatment is epinephrine; your illness was a life-threatening allergy. And that $300 price? That reflects a six-fold increase from a couple years ago. It’s one thing for medications to be expensive. But why does the same medication become more expensive over time?!? Americans are justifiably angry about rising prices for drugs that have been on the market for years. Many medications come to market at high prices, in part because it is expensive to identify, develop, and test new drugs. First, there’s the basic research. Admittedly, much of this work is funded by the federal government, but sometimes pharmaceutical companies pour significant money into such efforts too. Then there’s the cost of clinical trials – often hundreds of millions of dollars to test one drug, with no guarantee that the molecule being tested will work. When the trials go well, companies spend money and time (and remember: time is money!) jumping through regulatory hurdles, marketing their drugs, ramping up production facilities – this all adds up. It shouldn’t be surprising that pharmaceutical companies want to charge high prices for their products.

Paul Ryan is “excited” that the American Health Care Act, as Republicans call their bill, will trim the federal budget by several hundred billion dollars over the next decade. The 24 million people who are expected to lose insurance under the AHCA aren’t excited about the bill, which will cut government spending at their expense, with potentially fatal consequences for those who go without timely medical care.

Debates over healthcare reform often ask us to pick our poison. We either save money or we save lives.

But these debates ignore an antidote to this poisonous choice. If we tackle high healthcare prices, we can insure Americans at the same time as we curb healthcare expenditures.

This antidote is not theoretical conjecture. In fact, most developed countries provide universal insurance to their residents while spending far less per capita than the U.S. This affordable coverage exists in countries where healthcare payment is socialized, like the UK and Canada, and where it is privatized, like Germany and Switzerland. That’s because all these healthcare systems work to rein in high healthcare prices. As a result, appendectomies cost half as much in Switzerland as in America; and knee replacements cost 30% less in the UK than in the U.S.

Unfortunately, prices have been largely absent from healthcare reform debates in the U.S., whether those reforms are crafted by Democrats or Republicans. It’s true that politicians from both sides of the aisle occasionally speak out about pharmaceutical prices. Both Donald Trump and Hillary Clinton criticized pharmaceutical CEOs, like smirking Martin Shkreli, who made the news after enacting outrageous price hikes. But after a public scolding or two, discussion of pharmaceutical pricing usually ends.

Meanwhile, politicians rarely debate the often high price of hospital and physician services in the U.S., which constitute a much larger proportion of healthcare spending than do pharmaceutical products. When is the last time you heard a prominent politician question the lofty incomes of cardiologists, orthopedic surgeons or hospital CEOs?

Perhaps Republicans are hesitant to address high healthcare prices, so as not to galvanize special interests against their current legislation. But the American Medical Association already opposes the Republican healthcare plan, citing the harm vulnerable patients will experience “because of the expected decline in health insurance coverage.” The American Hospital Association also criticized the proposal for not “ensuring that we provide healthcare coverage” to the people dependent on subsidies for their insurance.

(To read the rest of this post, please visit Forbes.)

Donald Trump says he can improve upon the Affordable Care Act – promising to get everyone in the country “a much better healthcare plan at much lower cost.”

If that’s really what Trump wants to do, he should pay attention to one of the problems with Obamacare – the subsidies to purchase insurance might have been too stingy.

Let me explain. Before Obamacare, most people got insurance either with the help of their employers, or the government (if they qualified for Medicare or Medicaid). But some people had to buy insurance without such help, and the price of such coverage was usually – how do I say this nicely? – insanely expensive! Insurance companies charged extremely high prices for such policies, because they knew that many people shopping for such individual insurance were doing so because they were too sick to work, meaning their healthcare expenses would be higher than average.

Obamacare tried to make this kind of individual insurance more affordable. (They named it the Affordable Care Act for a reason!) The ACA accomplished this affordability, in part, by establishing insurance exchanges, which gave insurance companies a larger number of costumers to spread risk across, making it potentially easier for them to lower prices. In addition, Obamacare provided subsidies to people who otherwise could not afford insurance. The subsidies are quite generous for people with incomes close to the federal poverty level, and gradually diminish, dwindling to zero for people who make more than four times the federal poverty level. In other words, if someone’s family has an income near the federal poverty level, they get a lot of money to help them buy insurance. If a family makes 350% of the federal poverty level, they get a smaller subsidy. And if they make 450% of the federal poverty level, they don’t get any subsidy at all.

(To read the rest of this post, please visit Forbes.)

Knee replacements are booming. Between 2005 and 2015, the number of knee replacement procedures in the United States doubled, to more than one million. Experts think the figure might rise sixfold more in the next couple decades, because of our aging population. Since many people receiving knee replacements are elderly, Medicare picks up most of the cost of such procedures. In response to this huge rise in expenditures, Medicare is experimenting with ways to reduce the cost of procedures. But that raises a disturbing possibility. If orthopedic surgeons make less money on each knee replacement they perform, they might start performing unnecessary procedures.

Consider Medicare’s recent experiments with reimbursing knee replacements according to “bundled payments.” Under such reimbursement, Medicare gives healthcare organizations a lump sum to cover the cost of a knee replacement–not just the cost of the operation but also the cost of post-operative x-rays, physical therapy, even time in nursing homes or rehab hospitals. Before bundled payment, providers would receive separate payments for each of these services, meaning inefficient providers might take more x-rays than necessary, or keep patients in rehab hospitals longer than they needed such comprehensive care, and be rewarded for this inefficiency by receiving additional payments. Under bundled payment, Medicare tracks all the knee-replacement costs for a given patient, over a 90-day period. If a patient incurs fewer expenses than expected, Medicare gives the providers part of these savings back as a reward. (Warning–this is a very oversimplified description of bundling.) Early evidence suggests that bundled payments reduce the cost of knee replacements by an average of almost $1,200 per procedure. With a million such procedures performed in a year, that reduction could save over $1 billion. Moreover, these savings don’t seem to come at the expense of quality, at least as far as we can tell. (Quality measurement in healthcare is notoriously difficult.) For example, when knee replacements were paid for through bundled payments, there was no subsequent increase in readmission to the hospital or emergency room visits among patients whose procedures were reimbursed according to bundled payments. Same quality at a lower price–who could be against that?!

To read the rest of this article, please visit Forbes.

It used to be that hospitals billed Medicare for the services they provided, and Medicare – I know this is crazy! – simply paid the bills.

Those days are rapidly receding into history. Soon, a significant chunk of hospital revenue will be at risk, under a series of Medicare pay-for-performance programs. The idea behind P4P (as the cool kids call it) is simple. Third party payers, like insurance companies or the Medicare program, will monitor the quality of care offered by health care providers like hospitals. High quality providers will receive more money than low quality ones, thereby giving providers an incentive to improve the quality of care they provide.

Medicare has created several P4P programs which, unless they are halted by the Trump administration, are slowly coming into effect. By 2017, as I will show in a bit, these programs could put a sixth of Medicare payment at risk.

What are these programs?

One is the Hospital Value-Based Purchasing Program or (and you have to give Medicare folks kudos for their marketing prowess) VBP. Under VBP, Medicare monitors a bunch of quality measures, like the rate of hospital acquired infections, the number of patients falling while in the hospital, and even the risk adjusted mortality of hospitalized patients. Medicare scores each hospital based on how well it performs compared to other hospitals, and compared to its previous performance. This score determines part of a reward or punishment at the end of the year. By 2017, 2% of Medicare hospital payments will be redistributed according to VBP results, with money transferred from low to high performing hospitals.

Medicare has created another acronymically-challenged program, HRRP, which stands for Hospital Readmissions Reduction Program. The program measures how often patients with diagnoses like heart attacks, congestive heart failure, and pneumonia are readmitted to hospitals after an initial stay. The program will financially penalize hospitals that have excessive readmission rates.

Finally, under its HAC program (not named after the sound made by someone with bronchitis), Medicare is tracking how well hospitals reduce the rate of Hospital Acquired Conditions, like catheter-related bacterial infections. Some of these measures overlap with the VBP measures, amounting to a double counting. That’s a problem I’ll talk about in a minute.

(To read the rest of this article, please visit Forbes.)

My son was underperforming at school, and I was gently encouraging him to try harder (if gesticulating like an over caffeinated Italian qualifies as gentle encouragement). He could not understand why I was upset: “Dad, most of my friends are doing drugs and engaging in unprotected sex. You should be rewarding me for being such a good kid.”

“Reward you for not being bad?!?,” I replied incredulously. That made no sense to me. “When you go above and beyond – when you exert exceptional effort to achieve important goals – then we can talk about what reward you have earned.”

The folks running South Carolina’s Medicaid program don’t appear to agree with my parenting philosophy. A couple years ago, they contracted with a private insurer, the Centene Corporation, to manage its Medicaid population. Part of the company’s approach involved rewarding Medicaid enrollees for receiving recommended preventive care.

This rewards program flips medical payment on its head. Normally, when people go to the family medicine doctor for an annual checkup, they are charged a modest copay for the visit. But through its CentAccount program, the folks at Centene pay patients for receiving such care. You got that right – they aren’t charged for the visit; they are rewarded for it!

When a Medicaid enrollee brings her infant in for a Well Child visit, she receives $10. If she makes all six visits for the year, she will get $25 in that final appointment, adding up to a $75 reward from taxpayers for bringing her child to appointments that the rest of us brought our kids to at our own expense.

In fact, here’s a list of some of the healthcare services CentAccount rewards its customers for receiving:

At first glance, it might seem obvious that such rewards are unfair. For the same reason it seems wrong to reward my teenager for not doing drugs, why should we reward a parent for vaccinating a child – for doing what any good parent ought to do?

On the other hand, it is also not fair that many Medicaid enrollees are poor enough to qualify for the program despite working full time. It is also not fair that many lose out on their hourly earnings when they take time from work to bring their children to pediatricians.

(To read the rest of this article, please visit Forbes.)