A quarter of employers now offer only high-deductible insurance plans to their employees, and another quarter are thinking of following suit. The US is rapidly becoming a high out-of-pocket healthcare system, often with disastrous results. Consider what happened to Chris Howard after he saw the water in his toilet bowl turn bright red.

Howard (a pseudonym) figured it was probably from a hemorrhoid, but a colonoscopy test uncovered a Stage 3 cancer that had already begun invading the wall of his intestines. At the ripe young age of 38, Howard found himself face-to-face with a life-threatening illness.

To read the rest of this article, please visit Forbes.

MRI technologists move a patient from a MRI scanner at Wake Medical Center. Under a new program introduced by Blue Cross and Blue Shield, patients could receive cash rebates for choosing cheaper MRI facilities. N&O File photo.

Usually it costs money to get an MRI. But sometimes, in order to save money, insurance companies pay patients to seek less expensive medical care providers. Here is an excellent news report on the topic from The News & Observer:

North Carolina’s largest health insurer is proposing a solution to control runaway health care costs: paying people to use cheaper doctors and procedures.

Blue Cross and Blue Shield will offer customers between $25 and $500 per medical procedure for more than 100 procedures. The amount of the rebate depends on the procedure’s complexity and the cost savings of the cheaper option.

A Blue Cross spokesman pointed out that picking a cheaper option is more valuable than just the cash rebate.

“There is also the big cost-saving potential where you can shop, find a high-quality provider, and reallyreduceyourout-of-pocket costs,” said Blue Cross spokesman Austin Vevurka.

Insurers have for years sought to influence patient decisions through co-payments and high deductibles as a shared financial responsibility for medical costs. Blue Cross is taking the concept further by offering to share savings with the customer as a thank-you for reducing costs. In the past, this approach has been tried by financially rewarding doctors and hospitals for achieving cost savings.

Some health care experts are excited at the prospect of pulling back the veil on health care costs, saying that pricing transparency is long overdue. But others warn that using money to influence private medical decisions can be harmful, noting that not all doctors are equal.

“I would caution patients to be careful,” said Raleigh orthopedist Dr. Bradley Vaughn who operates at UNC Rex Hospital. “If someone saves $500 from a hip or knee replacement and suffers a serious complication, that $500 will be a drop in the bucket compared to all the misery they’ll experience.”

Blue Cross is offering the SmartShopper only to companies that pay for their employees health insurance and health care. In these instances, Blue Cross only administers the plan. There are nearly 400 such employers in North Carolina administered by Blue Cross and their plans cover nearly 1 million employees.

So far, 10 of those companies have opted to offer SmartShopper to their employees. Blue Cross, which covers 3.8 million people in the state, is not offering SmartShopper to patients on individual plans and other employer-sponsored policies at this time.

The State Health Plan, the largest Blue Cross customer in the state, has opted not to buy the SmartShopper service for the 727,000 state employees, teachers, retirees and dependents it insures. State Health Plan spokesman Frank Lester said the service “did not add any value.”

Nationwide, SmartShopper has generated more than $56 million in savings for employers and has paid out $6.7 million in cash incentives to employees in the United States in the past four years, according to Vitals, the New Jersey company that launched the technology in 2015. It’s used by 230 employers and more the 20 health plans with 2.5 million members around the country, company spokeswoman Rosie Mattio said.

Is it ethical?

Several medical ethicists praised SmartShopper as a technology that empowers the public on health care costs that have for far too long remained hidden in a black box.

“I like the idea of paying people to pay attention to what they’re doing because of the principle of responsibility — pay attention to the cost of your choices,” said Lance Stell, a retired philosophy professor at Davidson College who taught medical ethics to residents at Carolinas Medical Center. “We want patients to be empowered.”

And Dr. Peter Ubel, a physician and health sector management professor at Duke University’s Fuqua School of Business, made a different ethical point. “When a gastro-enterologist charges way more than another one down the street, nobody was raising ethical concerns about that, and yet you may be responsible for 20 percent of the cost.”

If you get health insurance through your job, beware: you might be picking up more of the cost of your medical care than you realize. With increasing frequency, employers are directing their workers to the kind of high deductible, high out-of-pocket insurance plans that leave workers financially responsible for a surprising portion of their healthcare expenses.

Not long ago, having insurance coverage meant your costs were largely covered. Americans could count on their employers to offer health insurance plans that covered the vast majority of their healthcare expenses. What’s more, employers even chipped in generously to cover a good chunk of people’s monthly premiums. As a result, Americans with good jobs could live their lives unafraid that they would be financially devastated by an unexpected acute illness.

Enter high out-of-pocket health plans.

On the surface, these plans look like bargains, because they cost less each month than other plans. When signing up for insurance, many people are attracted to these plans, knowing they will have less of their take home pay diverted to an insurance company. But then they discover that even a minor illness can turn that bargain to a burden.

(To read the rest of this article, please visit Forbes.)

American physicians dole out lots of unnecessary medical care to their patients. They prescribe things like antibiotics for people with viral infections, order expensive CT scans for patients with transitory back pain, and obtain screening EKGs for people with no signs or symptoms of heart disease. Some critics even accuse physicians of ordering such services to bolster their revenue.

So what happens when uninsured patients make it to the doctor’s office with coughs, low back pain, or other problems? Do physicians stop ordering all these unnecessary tests and services, out of recognition that most of these patients won’t be able to pay?

A study out of Harvard by Michael Barnett and colleagues provides a rigorous answer to this question. The researchers evaluated how often patients received any of a slew of unnecessary services. They compared patients with private insurance to those with Medicaid (which generally reimburses physicians much less generously than private insurance), and also to those with no insurance.

They found that almost 20% of privately insured patients receive unnecessary services, a staggeringly disturbing number. But even more disturbingly, the same percent of Medicaid enrollees and uninsured patients also receive unnecessary services.

In short, there’s way too much wasteful care, regardless of what kind of insurance people have (or don’t have).

(To read the rest of this article, please visit Forbes.)

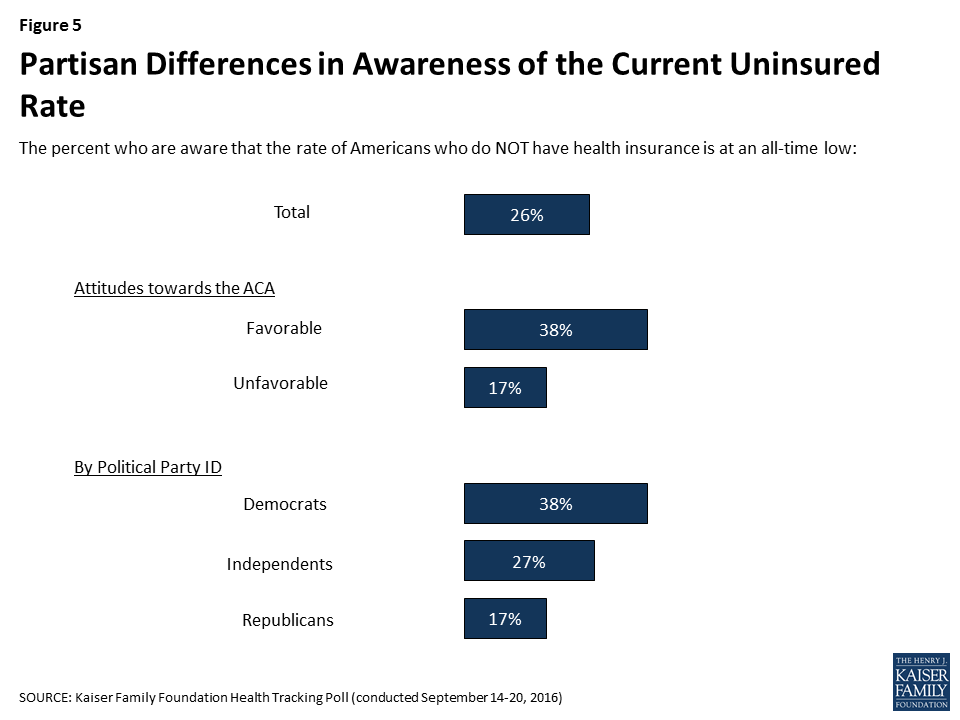

Obamacare dramatically reduced the number of people in United States who lack health insurance. Reduced as in: brought the proportion down to historical lows. Yet very few Americans knew this about the law, which is part of the reason why so many people didn’t like Obamacare. Here’s evidence to back up that connection, from the Kaiser Family Foundation:

Hard to like a law that hides its best features.

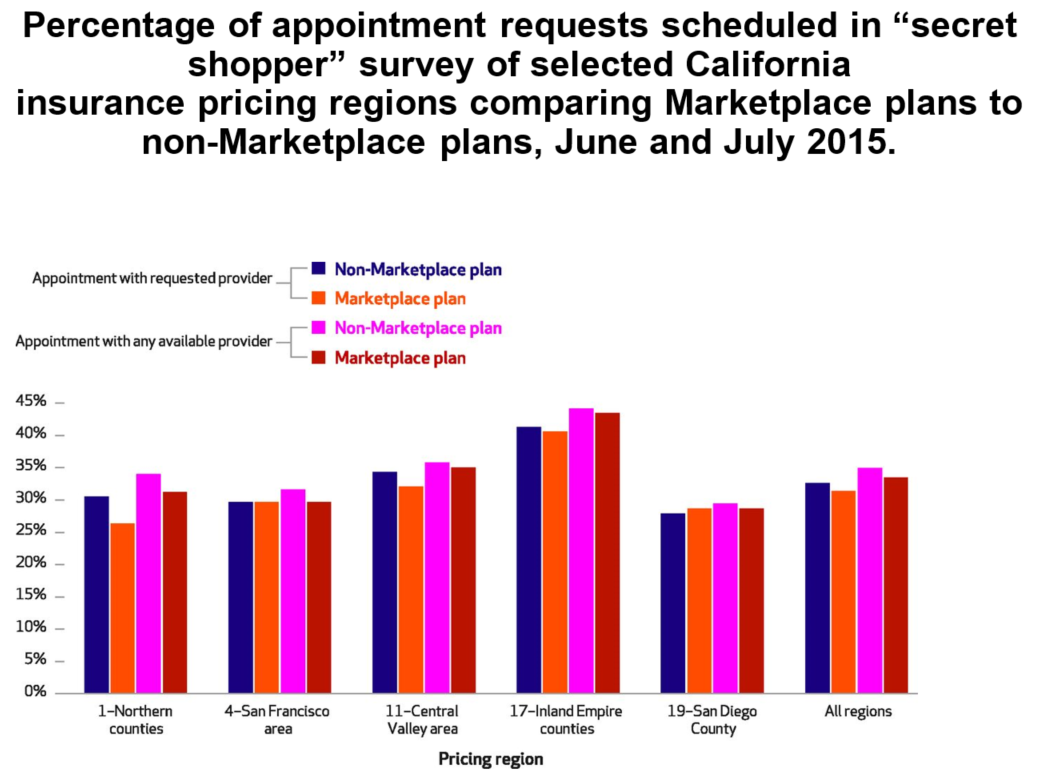

In a clever study, secret shoppers called primary care offices in an attempt to make a new patient appointment. People with Obamacare insurance, or “marketplace plans” in the below figure, had a hard time finding appointments. But so did people with traditional insurance.

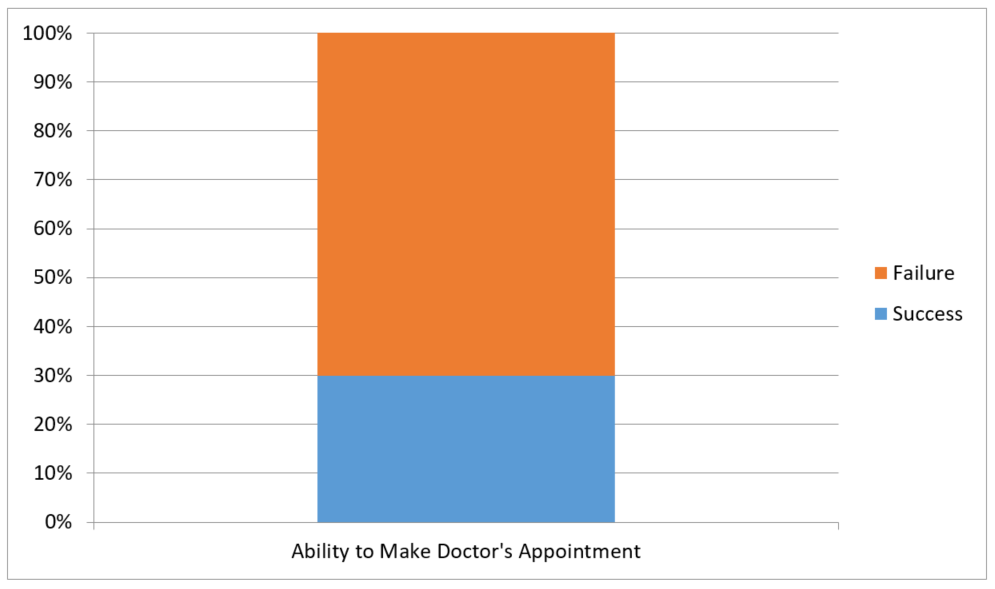

But there’s a bigger takeaway, one slightly obscured by the misleading y-axis, that doesn’t go all the way up to 100%. So here’s my over-simplified version of the study results:

That’s right – only 30% of people were able to make a doctor’s appointment.

Unacceptable!

Rep. Raul Labrador (R-ID) speaks with members of the media at Trump Tower December 12, 2016 in New York. / AFP / KENA BETANCUR (Photo credit should read KENA BETANCUR/AFP/Getty Images)

Back in May, an angry constituent asked Congressmen Raul Labrador why he voted for the Republican House Healthcare Bill, that the constituent claimed would cause people to die for lack of Medicaid funding. The Freedom Caucus member shot back with a now infamous retort: “Nobody dies because they don’t have access to healthcare.” Amidst backlash over what he now describes as an inelegant statement, Labrador tried to clarify his remarks: “I was trying to explain that all hospitals are required by law to treat patients in need of emergency care regardless of their ability to pay, and that the Republican plan does not change that.”

But Labrador forgot to mention that, although hospitals are required to treat emergently ill patients regardless of ability to pay, they are also allowed to bill those patients for that care. That means people without insurance often find themselves either avoiding emergency rooms altogether, or driving long distances to hospitals known for being more forgiving of medical debt. Labrador overlooked the life-threatening risks that financially strapped people take to keep out of medical debt.

Insurance sometimes saves lives by enabling people to get emergency care close to home, without fear of financial insolvency.

This travel-and-die phenomenon is not what most insurance enthusiasts think about when they say insurance improves health. Instead, they talk about how insurance makes people more likely to receive the primary care that prevents life threatening illnesses – mammograms and colonoscopies; blood pressure pills and flu shots. They point out that patients with insurance are more likely to see doctors when they start developing worrisome symptoms. With insurance, the cost of a cardiology appointment no longer stands in the way of getting that “heartburn” checked out. In short, insurance improves health and saves lives by being the difference between whether or not people receive lifesaving medical care.

(To read the rest of this story, please visit Forbes.)

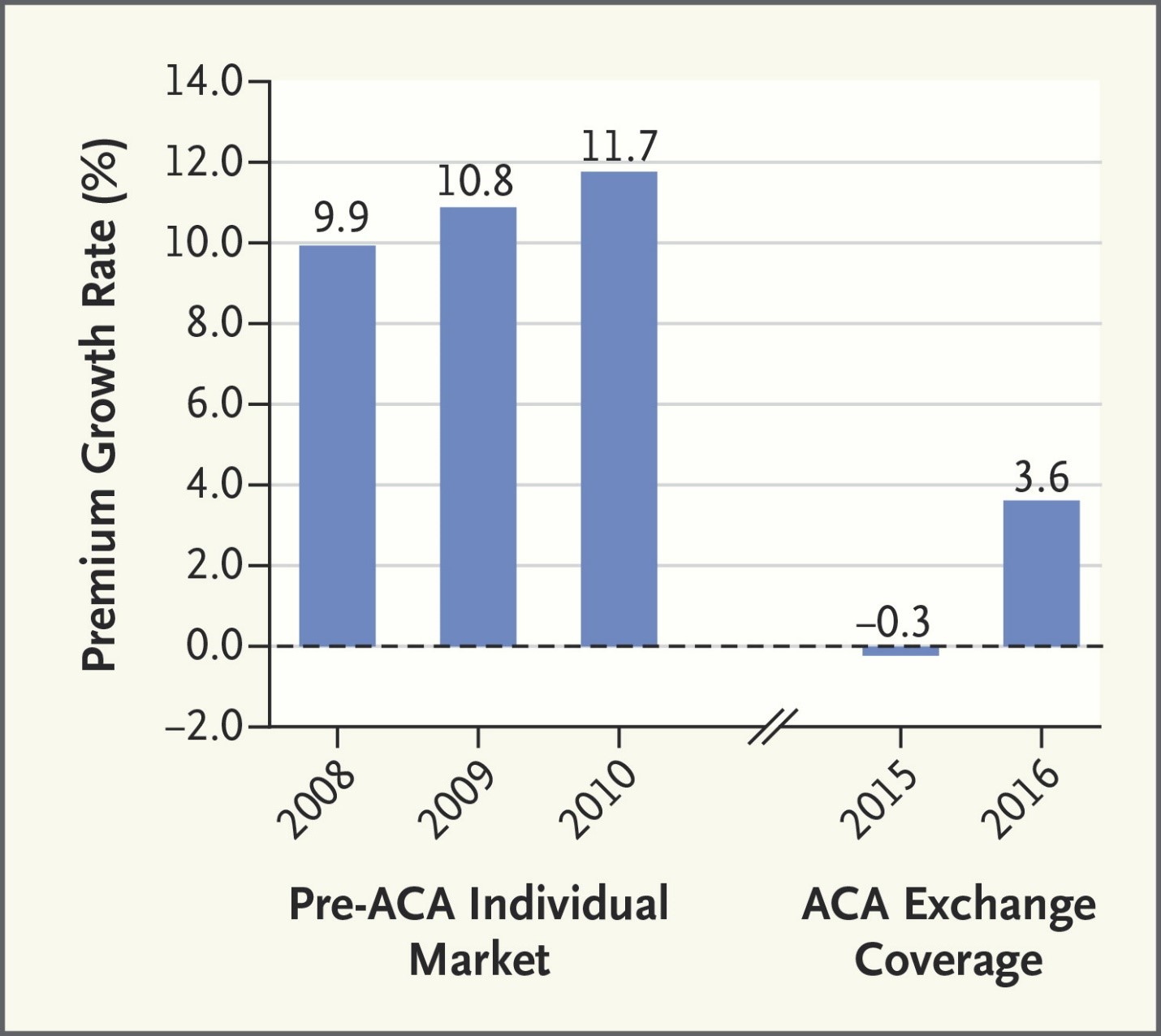

Here’s a picture from a New England Journal of Medicine article showing that in 2015 and 2016, Obamacare premiums grew more slowly than private insurance premiums rose before the law came into effect: New England Journal of Medicine

The Obamacare markets are new and unsettled. But so far they aren’t leading to runaway inflation. But what will happen to these markets if the Republicans are able to repeal and delay? Cue the ominous movie music!

Donald Trump says he can improve upon the Affordable Care Act – promising to get everyone in the country “a much better healthcare plan at much lower cost.”

If that’s really what Trump wants to do, he should pay attention to one of the problems with Obamacare – the subsidies to purchase insurance might have been too stingy.

Let me explain. Before Obamacare, most people got insurance either with the help of their employers, or the government (if they qualified for Medicare or Medicaid). But some people had to buy insurance without such help, and the price of such coverage was usually – how do I say this nicely? – insanely expensive! Insurance companies charged extremely high prices for such policies, because they knew that many people shopping for such individual insurance were doing so because they were too sick to work, meaning their healthcare expenses would be higher than average.

Obamacare tried to make this kind of individual insurance more affordable. (They named it the Affordable Care Act for a reason!) The ACA accomplished this affordability, in part, by establishing insurance exchanges, which gave insurance companies a larger number of costumers to spread risk across, making it potentially easier for them to lower prices. In addition, Obamacare provided subsidies to people who otherwise could not afford insurance. The subsidies are quite generous for people with incomes close to the federal poverty level, and gradually diminish, dwindling to zero for people who make more than four times the federal poverty level. In other words, if someone’s family has an income near the federal poverty level, they get a lot of money to help them buy insurance. If a family makes 350% of the federal poverty level, they get a smaller subsidy. And if they make 450% of the federal poverty level, they don’t get any subsidy at all.

(To read the rest of this post, please visit Forbes.)

Obamacare is a big, messy law with so many moving parts, it is often hard to tell how well it’s working. People debate whether it is killing jobs or creating them; they argue about whether it is lowering medical expenses or raising them. These debates often feel irresolvable because the law, being a national one, doesn’t allow for easy analysis. When an entire health care system changes in all 50 states simultaneously, it’s difficult to know what the world would have looked like if the law hadn’t existed.

That’s one reason the Obamacare Medicaid expansion is so interesting. You see, 19 states have refused to expand their Medicaid programs, leaving us with a kind of experiment – we can compare what happened in those 19 states with what happened in the other 31. That’s what Laura Wherry and Sarah Miller did in a study published in the Annals of Internal Medicine. In fact, that’s how we know that Obamacare causes diabetes.

Let me explain.

Wherry and Miller used data from the National Health Interview Study, looking at responses from people with incomes less than 138% of the federal poverty limit. In states that expanded Medicaid, all such people now qualify for healthcare coverage. But in states that didn’t expand, Medicaid eligibility is typically more stringent, as low as 75% of the federal poverty limit in some states. Wherry and Miller looked at data from before and after Obamacare expansions went into effect, to see how things changed in expansion versus non-expansion states. To read the rest of this article, please visit Forbes.